Your tax return might be a high point in your year, especially if you recently became a homeowner. Last year’s average refund was 11-percent higher than the previous year, totaling $2,775.* This number could increase if you own a home and have dependents or children.

Your homeowner’s tax guide for 2022: 6 big breaks + 3 more benefits

This year, the tax deadlines, at least, have returned to normal. The IRS started accepting 2021 tax returns on January 31, 2022, with the traditional filing deadline of April 15. Tax season may be more complicated for some, depending on how you were affected by the pandemic.

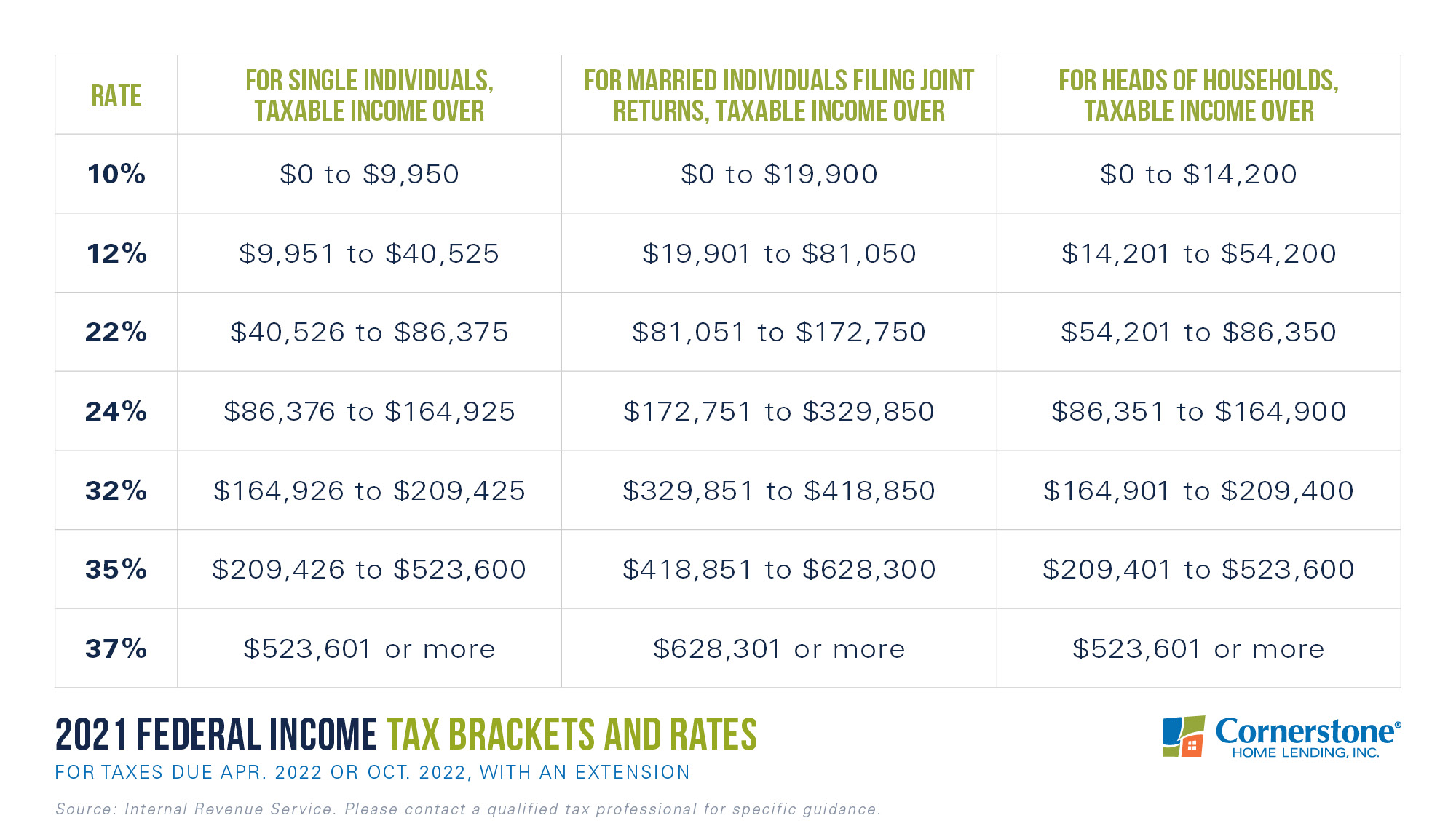

Accounting for annual inflation, tax brackets, as well as the standard deduction, rose for 2021 taxes filed in 2022:

As you’ve probably experienced, the recently reformed tax law lets consumers keep more money. Lower tax rates and a higher standard deduction make this possible. (Looking ahead, here’s where you can find the new standard deduction/brackets for the taxable year of 2022.)

With a higher standard deduction, there may be fewer taxpayers who itemize (list out expenses that can be subtracted from annual taxes). If you don’t have much to itemize, taking the standard deduction exempts two times as much of your earnings.

But if you own a home, itemizing some or all of these tax breaks could potentially bring more savings:

1. Home equity loan/HELOC interest.

- Now you can only deduct home equity interest that’s been used for renovations — a significant change from years past. But for those planning to renovate, this change to the 2018 tax law offers bigger benefits.

- If you’re eligible to deduct interest for renovations, that amount will go toward your total deduction limit of $750,000 in mortgage interest. (See below.)

- This kind of loan may be labeled as a home equity line of credit (HELOC), home equity loan, or second mortgage.

2. Mortgage insurance.

- You might be paying PMI (Private Mortgage Insurance) if you purchased a home with a conventional loan and put less than 20-percent down. This temporary-but-added monthly expense is deductible.

- While the PMI deduction was eliminated by the 2018 tax reform, it returned in 2020, allowing homeowners to take the deduction moving forward and retroactively for 2018 and 2019.

- There are restrictions: You can only claim this write-off if your home was purchased after 2006. If you recently refinanced, you may still qualify. You can also ask your loan officer about dropping your PMI, if you’re eligible.

3. Mortgage interest.

- The max for mortgage interest deductions lowered in 2018, dropping from $1,000,000 to $750,000. This deduction can include a secondary residence. Your secondary home can also be a condo, mobile home, or boat, though it’s a good idea to contact your CPA for details.

- For homes financed before December 15, 2017, the former deduction amount still applies.

- You’ll find all deductible mortgage interest on your Mortgage Interest Statement, or your lender-provided IRS Form 1098. States in which you have to file a state income tax return may allow you to write off your mortgage interest, even if you don’t itemize on your federal form.

4. Mortgage points.

- If you paid mortgage points — charged by your lender to decrease your interest rate — you can include them in your deductions. Point deductions may be limited for homes that cost over $750,000.

- You could deduct all your points at one time for the tax year they were paid. (If you bought a house in 2021, for example.) Or, you could deduct gradually, writing off a percentage of your points for every year you have your mortgage; deducting annually is required if you’ve recently refinanced.

- Each point is equal to 1 percent of your total loan amount. Note that loan origination points differ and are not deductible.

5. Some home improvements.

- Home renovations considered a medical expense, including equipment costs and fees for installation, could be fully deducted. (On a related note, you may be able to deduct unreimbursed medical expenses that exceed 7.5 percent of your AGI, or Adjusted Gross Income.)

- Examples of medically needed home renos include ramps, stairway and doorway modifications, support bars, new outlets or fixtures, and warning systems, as long as they don’t increase your home’s value.

- You could also get a credit for up to 26 percent of the cost of installing solar panels, solar water heaters, and other forms of solar energy.

6. State/local taxes.

- Tax reform also restricted deductions for state and local taxes (SALT). But the good news is that this write-off wasn’t eliminated.

- For taxes paid in 2021, the total deductible amount per taxpayer for property, sales, and income taxes is capped at $10,000. If you bought and sold a home last year, you could deduct a portion of your former property’s taxes.

- You should see a tax benefit in most parts of the U.S., except in higher-tax areas. But since a SALT deduction can only be used for a combo of state/local property taxes and either state/local sales or income taxes, itemizing can get complicated. This is another good time to consult your CPA.

While tax deductions help offset your taxable income, you may also be eligible for some tax credits, which help decrease how much you pay in taxes:

7. Child tax credit.

- If you’re a homeowner with children, you may appreciate that the max Child Tax Credit has doubled in recent years, and the American Rescue Plan Act, passed in 2021, has made it fully refundable.

- The credit has increased to up to $3,600 for each child who qualifies and may have more stringent income requirements; those who exceed the income limits may still be eligible for the former $2,000 Child Tax Credit.

- Since the Child Tax Credit increased as a result of the American Rescue Plan Act, many families were advanced direct payments during the 2021 tax year. If you received advanced payments – up to half of your total tax credit – this will be reflected when you file your 2021 taxes.

8. Recovery rebate credit.

- If you didn’t receive your third Economic Impact Payment (EIP) in 2021 in full, you could be eligible to claim the 2021 Recovery Rebate Credit (RRC), using Form 1040 or 1040-SR for seniors.

- The RRC amount for 2021 is $1,400 ($2,800 for married filing jointly), plus $1,400 for each dependent, up to the income limits of $75,000 ($150,000 for married filing jointly). Once these income limits are reached, the credit starts to decrease.

- Consult Notice 1444-C sent out via mail after the third EIP to determine how much stimulus payment you received in 2021. Note that the RRC is refundable. So, if it exceeds the amount of tax you owe, you could receive the excess as a refund.

9. Retirement contributions.

- Like the Child Tax Credit, deductions for retirement account contributions may not technically be homeowner-specific. But they’re probably going to apply. Recent tax changes have given anyone putting money toward retirement a bigger break.

- Limits on IRA contributions remain at $6,000 for those under 50, while max contributions for 401(k)s sit at $19,500.

- For taxpayers aged 50 and older, you can add $1,000 extra to your IRA contribution or $6,500 extra to your 401(k). You typically can’t contribute more than you make. There’s also a retirement Saver’s Credit of $2,000 ($4,000 for married filing jointly), as long as you meet income qualifications.

Still, there are a few home-related expenses you can’t deduct for 2021: HOA dues, home appraisal fees, homeowner’s insurance, and the cost of any home renovations that aren’t required for medical purposes. Most of these tax changes are enacted through 2025. And if you’ve started working freelance as a result of the pandemic, this may be the year to look into the home office deduction.

Can you cash in your tax return for a brand-new place?

As a homeowner, you may be getting more money back, and you could use these funds toward a new down payment. A bigger house. More outdoor space. Even a move to a more affordable zip code. Prequalify and find out what’s possible.

*“Filing Season Statistics for Week Ending October 22, 2021.” IRS, 2021.

For educational purposes only. Cornerstone Home Lending and its affiliates do not provide tax advice. Please consult your professional tax advisor for specific guidance.

Sources deemed reliable but not guaranteed.

You’re receiving this resource from your loan officer, who operates within the lending division of Cornerstone Capital Bank, a full-service financing institution.

Cornerstone Capital Bank is the parent organization that brings together multiple affiliated lending teams, providing shared resources, solutions, and long‑term support to help clients make confident financial decisions now and in the future.